Focus on USD & EUR

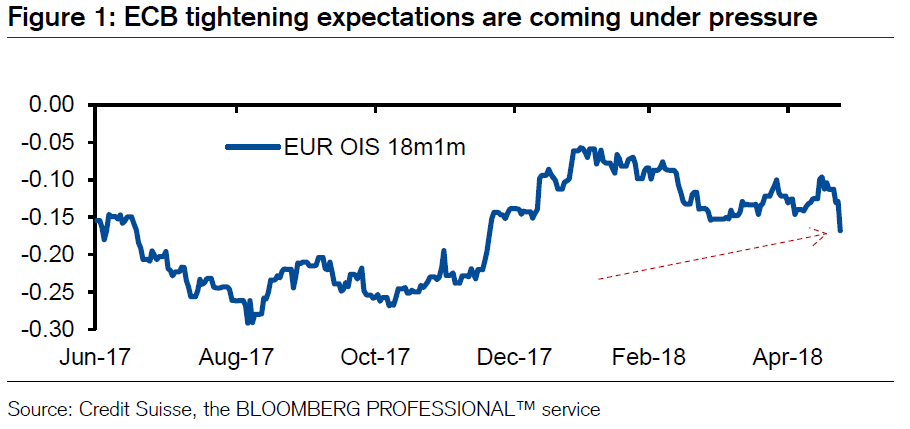

Our view on USD strength for the past few weeks has been that it is still too early to try to fade it. The deterioration in the preliminary May euro area PMI data, political risk in Italy and ongoing unease in EM space leave us unwilling to change course for now. The weak European data in particular complicates the fiscal equation for the periphery at a time when political risk is on the rise. We see a risk this could translate in more widespread negative impact on European assets, and see scope for ECB tightening expectations to come further under pressure ahead of the 14 June meeting. In terms of EURUSD, if the break below 1.1717 is confirmed, we would look for a move to 1.1675 initially but ultimately the risk is for a test of the November 2017 low at 1.1585.

We continue to favour being short EURCHF as an expression of intra-European political risk, and recommend adding a stop loss at 1.176 now that the pair has traded through the targets we set last week. Last week we had also highlighted the vulnerable setup for JPY crosses and stated that we would look to go short in the event of a break through 2018 lows. After today’s break, we recommend going short EURJPY targeting a move to the June 2017 highs at 125.82 and with a stop loss at 130.50.

EUR OIS - Future Interest Rate Pricing

Market Spotlight: A key inflection point for the EUR

We have been bearish on the EUR since the completion of a top earlier this year. EUR crosses are now at key inflection points, and are at risk of breaking lower to see the core trend for the EUR deteriorate further. A note of caution though, the Italian 10yr Bond Yield, a key driver of recent weakness, remains capped at crucial technical support, and we need to see a close to confirm the breaks we highlight below.

EURUSD has fallen sharply since the completion of a top, with the market now meeting the “measured objective” to this top and the 38.2% retracement of the entire 2017/18 rally at 1.1717/10. A closing break below here would see a more prominent bear leg emerge, with next meaningful support seen at 1.1554, the November low. If Italy breaks higher, there are further downside risks, and we would see support at 1.1449, with scope for the "neckline" to the medium-term 2017 base at 1.1335.

For EURJPY, our focus remains on the recent low and 38.2% retracement of the 2017/2018 uptrend at 128.95/85. A closing break below here would mark an important break lower and complete a large ‘head and shoulders’ top. Support would then be seen at the August low at 127.56, before the 50% retracement at 126.18, with scope for a move back at 123.65/50, particularly if Italy sees further weakness.

Finally, EURCHF’s rejection from the old SNB floor at 1.2000 has extended further to meet the "measured top objective” at 1.1724, with the market following through below here to remove the uptrend from April 2017 and 200-day average at 1.1700/1.1651. A close below here would mark a significant break lower, with the next meaningful support seen at 1.1482/47 – the 38.2% retracement of the 2017/18 rally and year to date low. The next cluster of support below here is seen at 1.1318/1.1259.

The team at Core is passionate about investing.

Get in touch with us today.