House View: Add Value Through Broad Diversification

Globally synchronized economic upswing supporting financial market performance

So far, the year 2017 has been a very good year for investors. Global equity markets produced double-digit returns and fixed income indices have also performed positively. This performance is largely supported by a globally synchronized economic upswing, while at the same time, inflation has stayed surprisingly low giving central banks the leeway to reduce accommodation only very gradually.

Still positioned for robust growth

Going forward, global growth is likely to remain robust as credit growth and investment spending have picked up. And while inflation is likely to pick up somewhat, it is likely to stay very low in a historical context. So, in our House View, we are still positioned for growth. We have a positive view on commodities, which are the most sensitive to economic growth, preferring energy over precious metals. In equities, valuations are a concern following the significant rally, even considering the robust growth outlook. So, while we do not expect a major correction, an outright positive view seems too risky at this stage. We are neutral overall equities and real estate. In a similar fashion, we are neutral fixed income. While bond yields are low,

bonds can serve as a safe haven in case of negative surprises, and with inflation likely to stay on the low side, downside risks seem contained. So, at the overall asset class level, we favor a broadly diversified portfolio with some tilt toward growth, reflected by our positive commodity view.

Adding alpha through differentiation within asset classes

While we are neutral overall equities and bonds, this does not mean that there are no investment opportunities. In fact, we favor a broad differentiation within asset classes. In equities, we prefer markets that are either less overvalued or have strong growth rates. On the regional side, that means we prefer

Japan, EMU, Switzerland, and Australia over the USA and the UK. On the sector side, we prefer energy, healthcare and telecom over consumer staples and industrials. In fixed income, we believe there are good opportunities in investment grade and financial bonds. In currencies, we think the CAD and the GBP can appreciate against the USD as central banks in these countries become more hawkish.

Central banks slowly proceed with normalizing policy

Most major central banks have continued along their path of normalizing policy in recent months, with some tendency to surprise on the hawkish side: the Bank of Canada (BoC) raised rates twice already this year and may deliver another hike in October; the Bank of England (BoE) seems to be at the verge of a rate hike; and the US Federal Reserve (Fed) also moved quicker on both rates and the balance sheet than expected at the beginning of the year. Others, such as the European Central Bank (ECB) are proceeding more cautiously, while there appears to be little appetite yet to change monetary policy at the Bank of Japan.

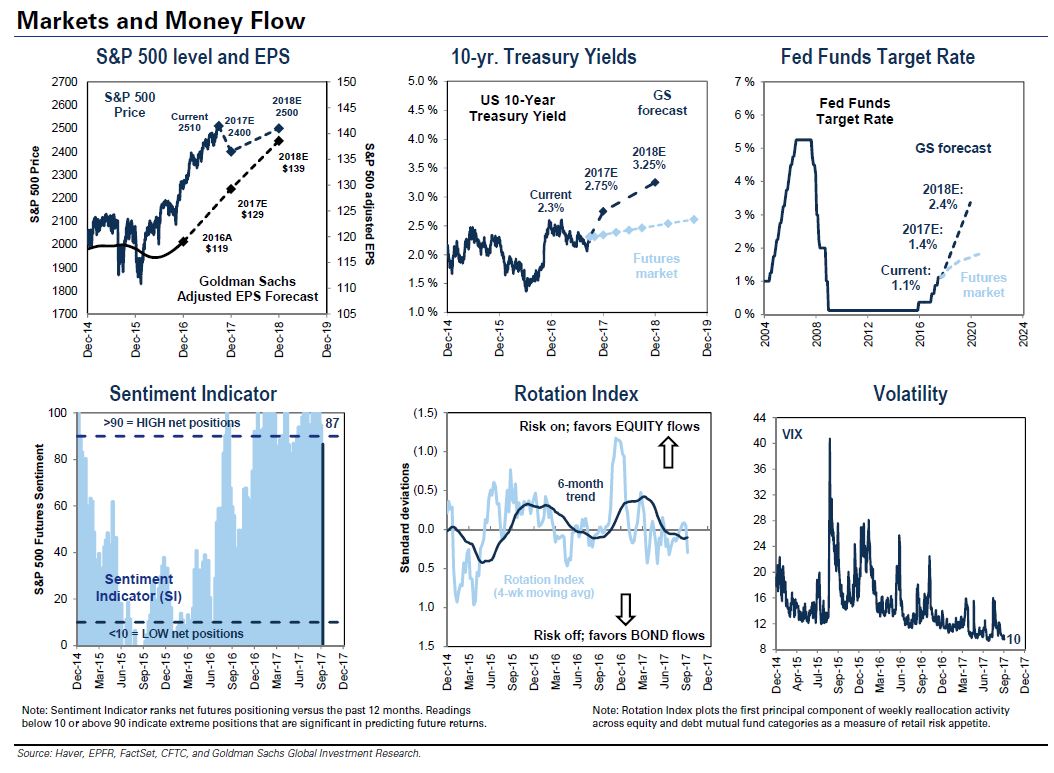

Markets & Money Flow

The team at Core is passionate about investing.

Get in touch with us today.