Global Macro

Macro recovery in Europe and the prospect of reforms in the Eurozone are the highlights, together with better cyclical data in China.

Helpful context for central banks to slowly normalize monetary policy.

Chart - Citi Eurozone Eco Surprise Index - Positive Surprise Continuing

Fixed Income

Sluggish US data now tempers the prospect of higher yields. We move US Treasuries to neutral relative to other regions.

Chart - US 10Yr Yields

Equities

The US market still looks most expensive and 'overcrowded' and provides the best place to raise cash from.

Eurozone, Canada, Australia and Switzerland are our preferred regions.

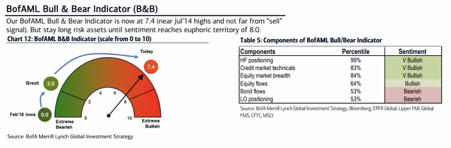

Chart - Bullish Sentiment Near Extremes

Forex

USD weakness a thread across markets. Given weaker macro and price momentum, we neutralize EURUSD, USDCHF and AUDUSD.

The ECB's unchanged rhetoric may reflect some sensitivity to the FX rate, but no alarm.

Chart - USD Continuing Downtrend

Strategy

Risk appetite is high, global growth is solid and so far the US earnings season is delivering.

Notably, growth momentum is better in Europe and China than the USA.This and the newfound tendency for central banks such as the Bank of England and Swedish Riksbank to contemplate less accommodative monetary policies has helped currencies other than the USD to gain momentum. In addition, the political risk premium in foreign exchange has shifted from Brussels to Washington. In this context, the USD has had one of its sharpest six-month dips in recent decades.

This has helped US exporters and propelled the Nasdaq to new highs. Yet, the lack of an outright sanction of recent EUR strength by ECB President Mario Draghi may embolden buys, and we have neutralized our EUR view.

The team at Core is passionate about investing.

Get in touch with us today.